May 2026 – Earnings Reassert the Narrative

Key takeaways:

- April’s powerful equity rebound was not simply a relief rally — it was validated by the strongest corporate earnings growth since Q4 2021, with nine of eleven S&P 500 sectors posting year-over-year gains. The underlying health of corporate America remains a compelling foundation for patient, long-term investors.[1]

- The AI capital expenditure cycle has broadened the earnings story well beyond technology. Combined hyperscaler capex of approximately $725 billion in 2026 is generating meaningful tailwinds for Industrials, Materials, and Utilities — a dynamic that supports our active managers’ ability to find opportunity across the market, not just in the names that dominate the headlines.[2]

- The Federal Reserve’s leadership transition introduces a new variable that warrants close attention. With Kevin Warsh expected to assume the Chair role as early as the week of May 11, the June FOMC meeting will be closely scrutinized for any shift in tone — and with four dissenting members and Chairman Powell remaining on the Board, the path to easier policy is less clear than markets may be assuming.

[1] Bloomberg, monthly total return data, April 2026.

[2] FactSet, “Earnings Insight,” 1 May 2026.

The drama that defined the first quarter — Operation Epic Fury, the closure of the Strait of Hormuz, and Brent crude’s surge above $119 per barrel — gave way in April to one of the most powerful monthly equity rallies of the past several years. The catalyst arrived on April 8th, when the United States and Iran agreed to a Pakistan-brokered ceasefire that paused active hostilities and committed both sides to reopening the Strait. With the immediate energy panic subsiding, markets refocused on the fundamental story we have argued was being overlooked: corporate profits are growing at the fastest pace since the post-pandemic rebound, and the AI capital expenditure cycle has scaled to a level that meaningfully impacts industries far beyond technology.

Markets & Geopolitics: A Powerful Reversal

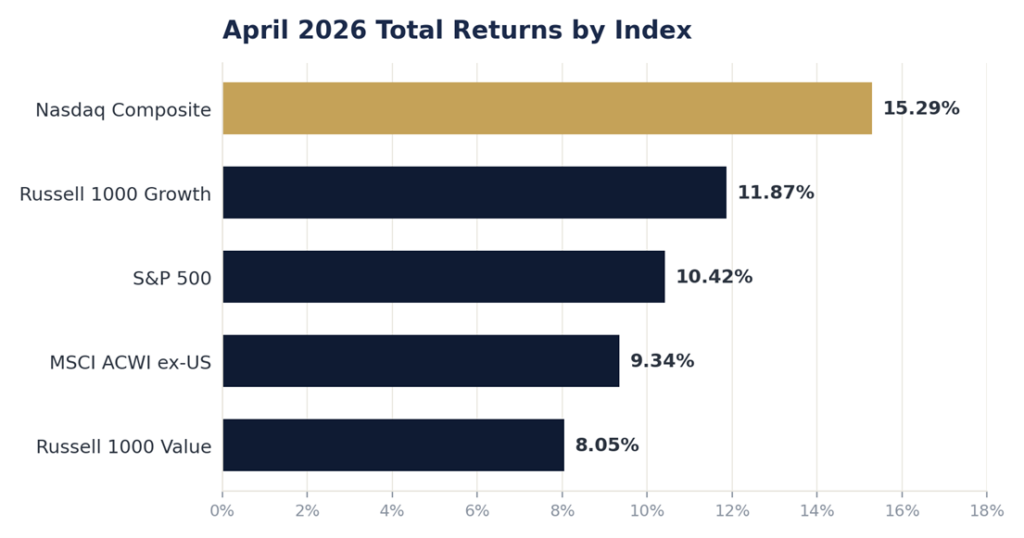

April produced a near-complete reversal of the leadership patterns that defined the first quarter. Growth meaningfully outpaced value, with the Russell 1000 Growth Index returning 11.87% versus 8.05% for the Russell 1000 Value Index, and the Magnificent Seven — which had collectively shed over $2 trillion in market capitalization during the first quarter — were among the largest contributors to April’s rally. International equities also participated as the energy panic receded, with the MSCI ACWI ex-US Index returning 9.34%. That said, the situation in the Middle East remains far from resolved. Subsequent talks between Vice President Vance and Iranian counterparts failed to produce a durable framework, the U.S. has maintained a naval blockade of Iranian ports, and Brent crude finished April above $114 per barrel — well below its February peak above $119, but meaningfully elevated relative to the roughly $61 level that prevailed pre-conflict. We continue to view geopolitical risk as one of the most underappreciated tail risks in the current environment.

Earnings: Broad Strength, Led by AI Capex

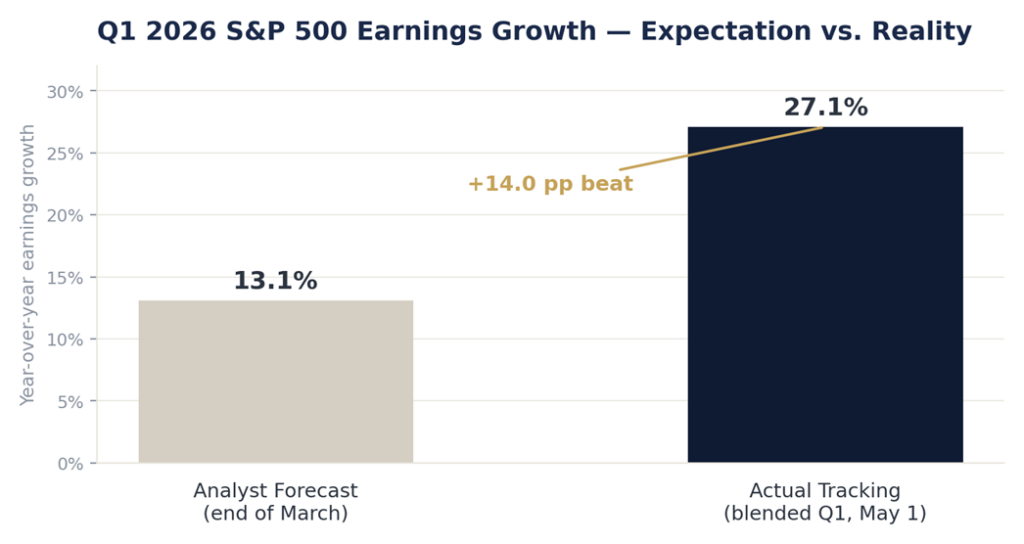

While the ceasefire provided the catalyst, April’s rally was ultimately driven by the strength of first-quarter earnings. With nearly two-thirds of the S&P 500 having reported, earnings are tracking 27.1% year-over-year growth — a substantial step-up from the 13.1% growth rate analysts had projected at the end of March, and the strongest reading since the post-pandemic surge in Q4 2021. Nine of eleven sectors are posting year-over-year earnings growth, and revenue growth of 11.1% would mark the strongest top-line print since Q2 2022. Much of this is being driven by an AI capital expenditure cycle that has reached a scale we believe is materially underappreciated. Combined 2026 capex guidance from Alphabet, Amazon, Meta, and Microsoft now totals approximately $725 billion, up from roughly $410 billion in 2025, with all four management teams signaling that 2027 spending will move materially higher. The result has been a powerful tailwind not just for semiconductors and software, but for sectors such as Industrials, Materials, and Utilities — a development we believe has important implications for portfolio construction.

Federal Reserve: Dissent and Transition

April was also a notable month for U.S. monetary policy. The FOMC held the federal funds rate steady at 3.50%–3.75% for a third consecutive meeting, citing elevated uncertainty stemming from the Middle East conflict. The decision drew unusual dissent — four members voted against the action, the most divided FOMC since 1992. More significantly, Chairman Powell, in his final press conference as Chair, announced he intends to remain on the Board of Governors after his term concludes on May 15, citing concerns about institutional independence. Kevin Warsh, President Trump’s nominee, has advanced from Senate Banking and could be confirmed as early as the week of May 11. The June FOMC meeting will likely be the first under Warsh’s leadership, and we will be watching closely for any shift in policy direction. Given the existing reluctance among committee members to support further easing and Powell’s continued presence on the Board, we believe a rapid pivot to a meaningfully more dovish stance is unlikely in the near term.

Looking Ahead & Positioning

In last quarter’s commentary, we observed that investor sentiment had become singularly focused on the Middle East conflict, with the underlying strength of corporate fundamentals largely overlooked. Within a matter of weeks, that dynamic has fully reversed. As we move beyond the bulk of earnings season, the tailwinds that supported April’s rally may begin to fade. Forward consensus now calls for earnings growth of 21.3% in Q2 and 20.6% for the full year — robust expectations that leave limited room for disappointment. Our balanced approach across asset classes, geographies, and styles remains the foundation of client portfolios, and our active managers — who emphasize fundamentals, valuation, and prudent risk management — remain well positioned for the current environment. The rapid recovery of risk appetite, the narrowing margin for error in earnings expectations, and the unresolved geopolitical and policy backdrop all argue for continued discipline rather than complacency.

We welcome the opportunity to speak with each of you about your portfolio’s performance, our current positioning, and any aspect of the market environment you would like to discuss in greater detail.

For additional information, please contact Mason Williams, Chief Investment Officer / Managing Director, at 786-497-1214, or Michael Unger, CFP® , AEP®, Senior Vice President / Investment Officer, at 786-292-0310.